Get educated on Apple with this summary of Horace Dediu’s analysis of Apple’s Fiscal Second Quarter 2026 performance. It highlights a company in a state of high-growth acceleration, driven by a “super cycle” in hardware and a foundational surge in Services, while navigating a significant leadership transition.

Executive Summary

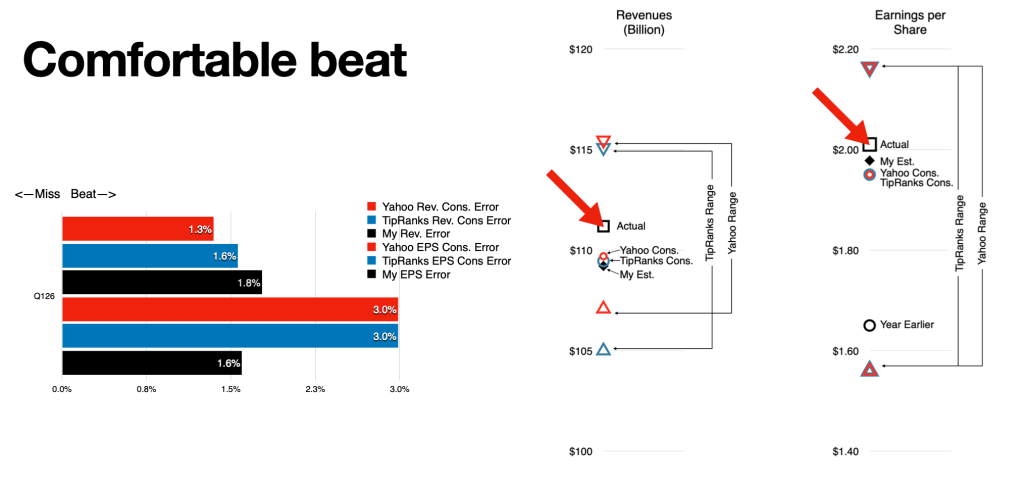

Apple delivered a “comfortable beat” on both revenue ($105B–$115B range) and EPS. The core narrative is the divergence of hardware and services: while the iPhone 17 is driving a 22% growth surge due to a new form factor and “orange color” appeal, the Services segment is providing a stable, high-margin (nearly 80%) floor that keeps users locked in.

Crucially, Dediu identifies a shift in corporate DNA: Apple is now an engineering-led company under new CEO John (Ternus), evidenced by R&D spending approaching 8% of sales and a sudden, “out of character” pivot away from aggressive stock buybacks.

Key Insights & Financial Data

- Segment Performance:

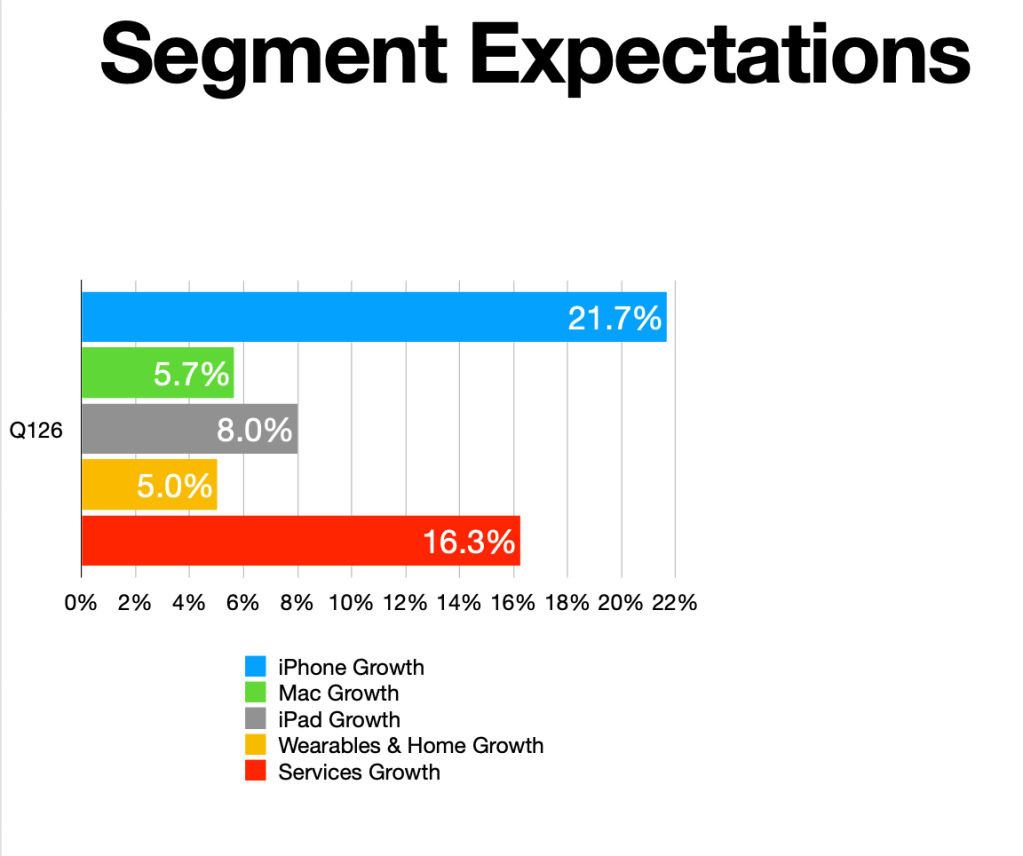

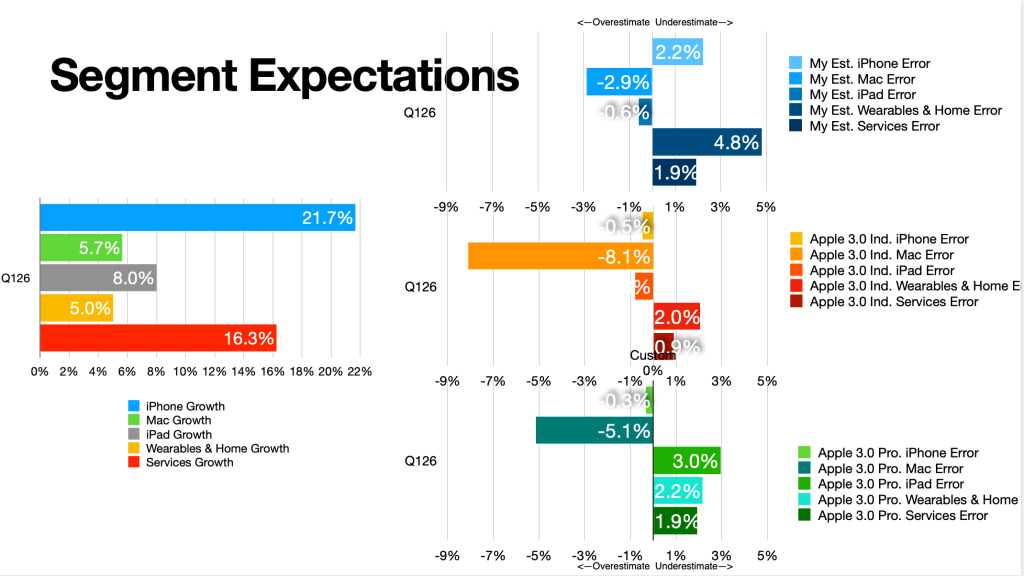

• iPhone: 22% growth (comparable to holiday peaks).

• Services: 16% growth; foundational to ecosystem retention.

• Mac: 5.7% growth (underperformed expectations due to late-quarter product launches like the Mac Neo). - The “Unbelievable” Margins: Gross margins are flirting with 50%, a level not seen in 15 years. This is fueled by Services margins approaching 80%, mimicking the “money printing” software models of 1990s Microsoft.

- Capital Allocation Shift: Buybacks halved from $25B to $11B. Dediu notes that Apple has effectively abandoned its “net cash neutral” goal, suggesting the new engineering-focused leadership prefers holding cash or reinvesting over returning it to shareholders.

- The Engineering Culture: R&D has overtaken SG&A. Dediu argues Apple is now a fundamental research powerhouse, necessitating a CEO who is an “engineer’s engineer.”

Critique

Strengths: The “Asymco” Edge

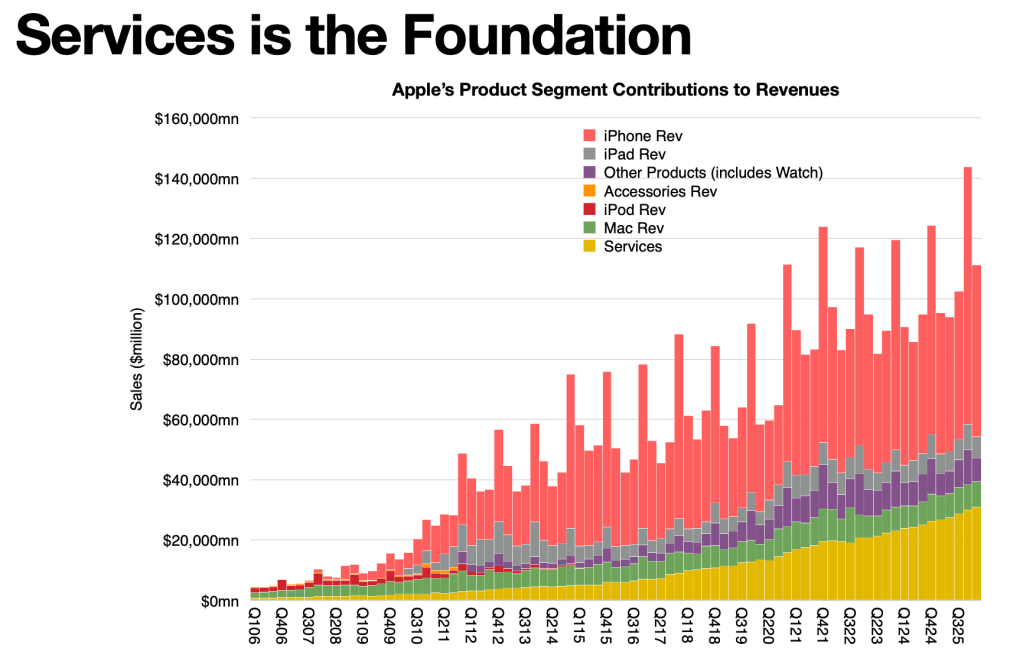

- Structural Analysis: Dediu excels at looking past the “spikes” to see the “pulse.” His observation that Services is the “tide that lifts the boats” rather than just an add-on is a sophisticated take on ecosystem stickiness.

- Leadership Archetypes: His analysis of the CEO transition, contrasting Tim Cook’s operational focus with John’s engineering focus, provides a cultural explanation for the shift in capital allocation (R&D spend vs. Buybacks) that numbers alone might miss.

- Installed Base Focus: By tracking “new to product” metrics (especially in India), he focuses on the long-term health of the ecosystem rather than just quarterly units.

Weaknesses: Potential Blind Spots

- The “Orange Phone” Simplification: While Dediu acknowledges the “super cycle,” attributing 22% growth largely to a “distinctive-looking product” or a specific color (orange) may be reductive. It glosses over macroeconomic factors or the “Claude bots” and AI integration (the “Neo” and “agentic” shift) he briefly mentions.

- Speculative Causation on Buybacks: He links the drop in buybacks directly to the new CEO’s personal philosophy. While plausible, this ignores other possibilities: the stock price being “asymptotic” (too expensive), high interest rates, or a strategic “war chest” for M&A in the AI space.

- The “Engineering Welfare State” Risk: He warns about engineers chasing “pipe dreams” but doesn’t reconcile how this fits with Apple’s historical reputation for ruthless product curation. If R&D is vertical, the risk isn’t just “navel-gazing”; it’s a loss of the operational efficiency that defined the Cook era.

Forward Outlook (Q3 2026 Guidance)

Dediu expects the acceleration to continue:

- Revenue Growth: ~16% ($108.7B).

- EPS Growth: ~22% ($1.92).

- Mac Recovery: He predicts an 18% bounce for Mac as “Neo” supply stabilizes.

- Investment Sentiment: Price targets are consolidating above $310, reflecting a market that is finally “getting excited” about the hardware/service synergy.